The State of AI in Australian Logistics: 2026 Update

Only 50% of Australian fleet managers use AI tools. The gap between leaders and laggards is widening. Here's where the industry stands in 2026 and what's actually delivering ROI.

The Numbers Tell the Story

Australian logistics is a $158 billion industry at a digital inflection point. The market is projected to reach $275 billion by 2035 (5.7% CAGR), driven by e-commerce growth, population increases, and supply chain complexity.

But the technology adoption picture is uneven:

| Stat | What It Means |

|---|---|

| Only 50% of fleet managers use AI tools | Half the market is still untapped |

| 60% cite legacy systems as their top barrier | The problem isn't willingness — it's infrastructure |

| 74% say workforce isn't ready for digital tools | Technology is ahead of adoption capability |

| Only 40% report measurable AI improvements | 60% need help getting value from AI investments |

| 81% expect tech to cut freight costs by 5%+ by 2030 | Budget intent exists |

The gap between leaders and laggards is widening. Companies that adopted AI early are seeing compounding returns — better data, better models, better decisions — while those who haven't started are falling further behind.

Five Triggers Driving Adoption in 2026

1. Mandatory Emissions Reporting (AASB S2)

The single biggest catalyst. From FY26, entities above $500M revenue must report climate-related disclosures including Scope 3 emissions. By FY29, the threshold drops to $50M, pulling in thousands of logistics operators.

Even companies below the threshold are affected: their customers who are reporting need per-shipment emissions data from their logistics providers. Can't provide it? Lose the contract.

2. Labour Shortages

Driver shortages, warehouse worker shortages, and admin staff shortages continue to worsen. The average age of a heavy vehicle driver in Australia is 47. Automation isn't replacing workers — it's filling gaps that can't be filled any other way.

3. Legacy System End-of-Life

60% of logistics operators cite legacy systems as their top digital transformation barrier. Systems built 10-15 years ago are reaching end-of-life: vendors have stopped supporting them, security patches aren't available, and they can't integrate with modern tools.

4. Customer Expectations

The "Amazon effect" hasn't slowed down. B2B customers now expect the same visibility, speed, and accuracy they get as consumers. Real-time tracking, API integration, per-consignment reporting — these are table stakes for enterprise contracts.

5. Government Incentives

The AI Adopt Program ($3-5M grants for SME AI adoption), CRC-P Round 19 (up to $3M for AI-focused projects), and the Victorian Freight Sector Innovation Fund ($8M for low-emission tech) are making AI investment more accessible for mid-market operators.

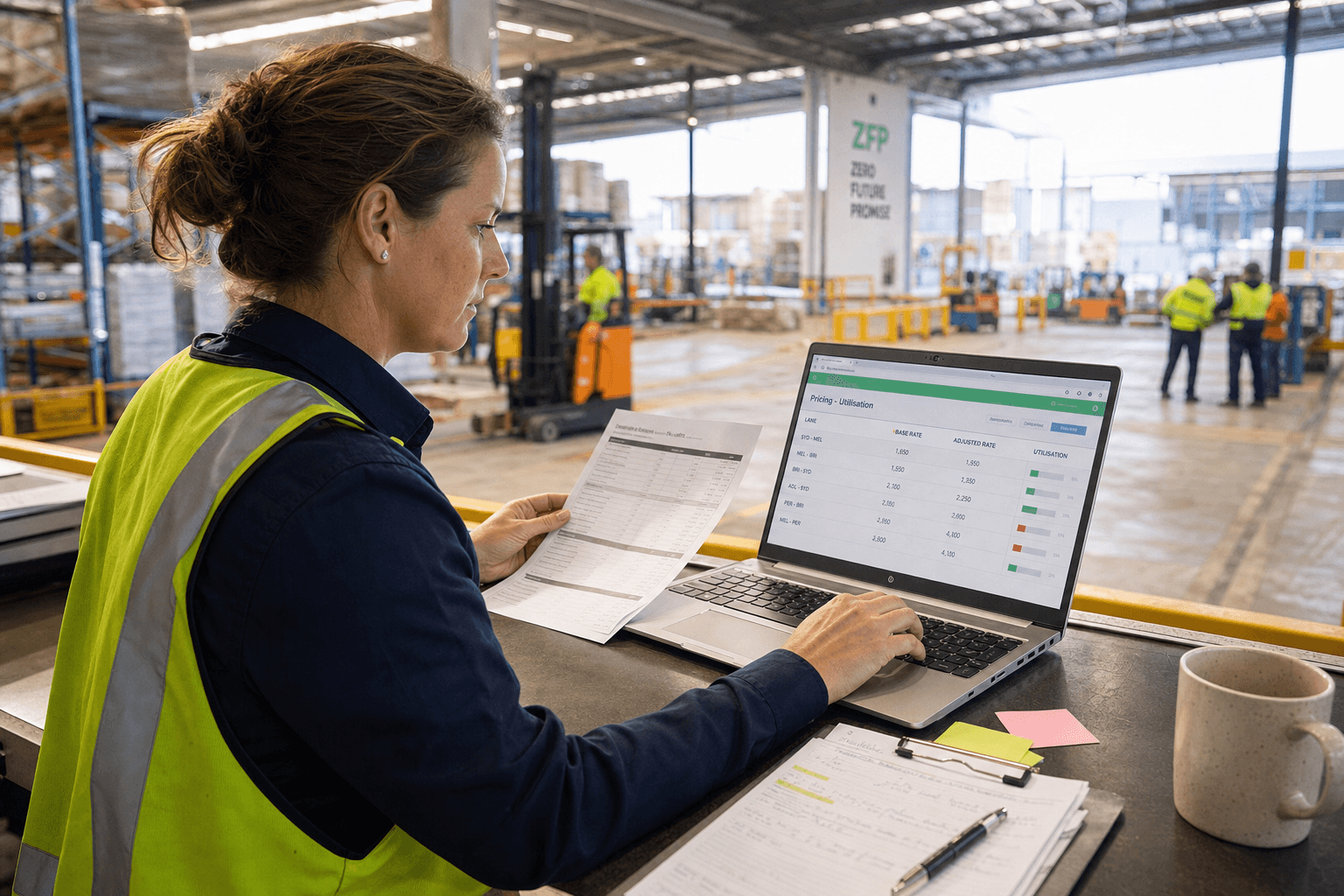

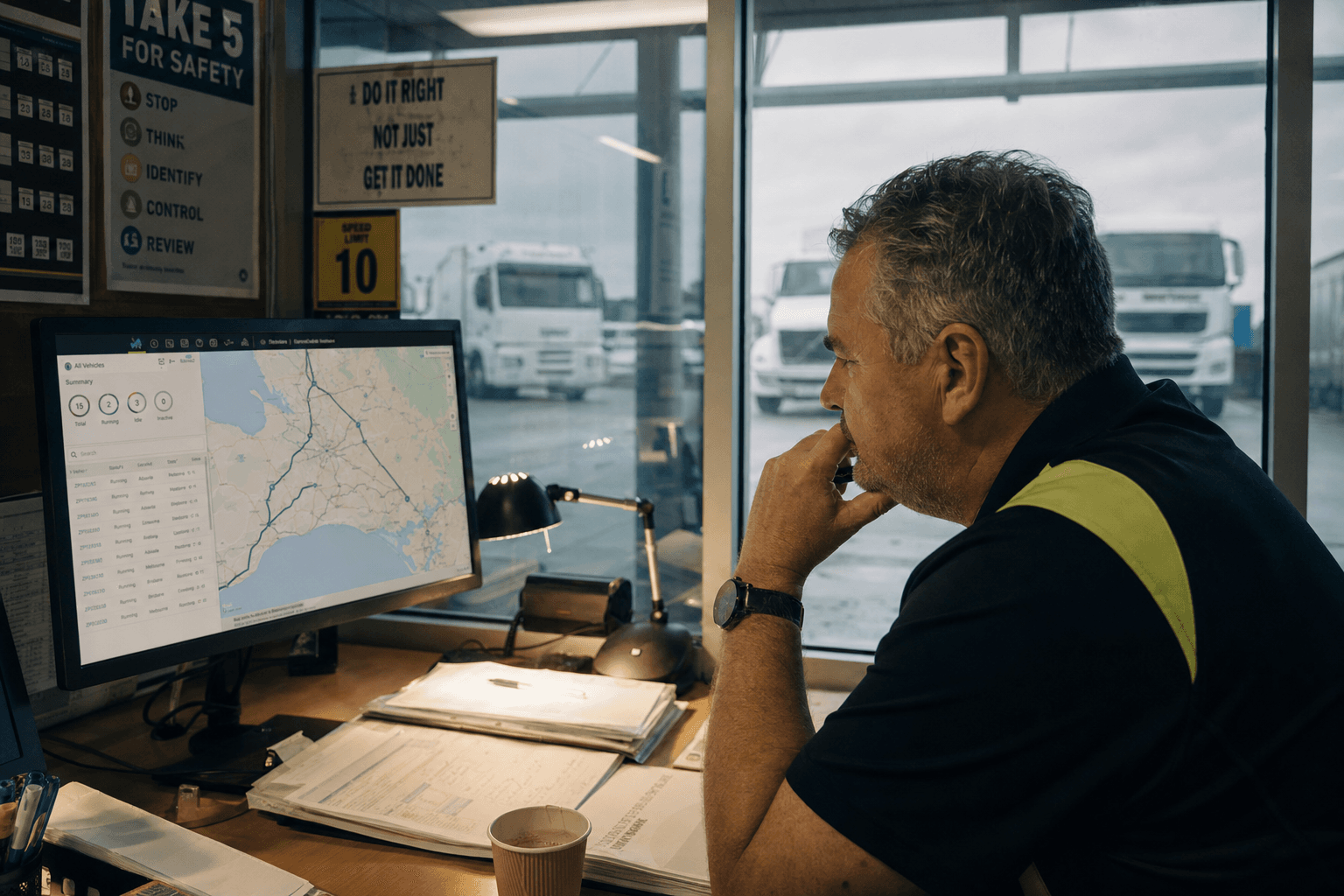

What's Actually Delivering ROI

Not all AI applications are equal. Based on what we're seeing across the Australian market, here's where the proven ROI sits:

Tier 1: Proven ROI (Payback <12 months)

- Route optimisation: 15-25% fuel cost reduction. Mature technology, well-understood implementation path.

- Document intelligence: 90% reduction in manual data entry. Clear before/after metrics.

- Freight invoice auditing: 2-5% cost recovery on carrier spend. Pays for itself in months.

Tier 2: Strong ROI (Payback 12-24 months)

- Demand forecasting: 15-30% improvement in resource utilisation. Requires 12+ months of historical data.

- Emissions tracking automation: Saves 60-80 hours per quarter in manual reporting. Also protects revenue from contract requirements.

- Predictive maintenance: 70-80% reduction in unplanned breakdowns. Requires telematics investment.

Tier 3: Emerging ROI (Early stage, case-by-case)

- Autonomous last-mile: Technology improving but regulatory framework incomplete in Australia.

- Digital twins: Powerful for warehouse optimisation but high implementation cost.

- Generative AI for customer service: Promising but requires significant training data.

The Mid-Market Gap

The biggest opportunity — and the biggest problem — is in the mid-market.

Enterprise operators ($500M+ revenue) have internal technology teams and large consulting budgets. They're adopting AI systematically.

SME operators can use off-the-shelf platforms with built-in AI features that work well for standard operations.

The mid-market — regional carriers, 3PLs, warehousing operators with $20M-$500M revenue — is stuck:

- Too big for off-the-shelf platforms (their operations are too complex or specific)

- Too small for large consultancies ($500K+ engagement minimums)

- No internal tech teams to build solutions themselves

- Legacy systems that can't integrate with modern tools

This is where the real opportunity sits. The mid-market needs a trusted partner to guide AI adoption — someone who understands logistics operations and can build solutions that work with existing systems.

Many Australian logistics companies are still running on legacy systems that weren't built for AI integration, creating the 60% barrier mentioned in our research. For fleet operators ready to bridge this gap, conducting an AI readiness assessment is often the first practical step before implementing solutions like route optimisation that deliver measurable ROI.

What to Do Next

If you're a logistics operator who hasn't started with AI:

- Don't boil the ocean: Pick one problem, solve it, measure the result, then expand. Route optimisation or document intelligence are good starting points.

- Start with your data: The biggest barrier to AI isn't technology — it's data. Understand what data you have, where it lives, and how clean it is.

- Talk to your customers: What are they going to require from you in 12-24 months? Emissions data? API integration? Real-time visibility? Work backwards from their timeline.

- Check government grants: The AI Adopt Program and state-level innovation funds can offset 30-50% of implementation costs.

The companies that start now will have 12-24 months of learning, data, and capability when the broader market catches up. That's a significant competitive advantage in an industry where margins are thin and switching costs are high.

Get a free AI readiness assessment for your operation →

Ready to assess where your logistics operation stands on AI adoption? We help Australian fleet managers move from laggard to leader with practical, ROI-focused implementations. Get in touch to discuss your specific challenges and opportunities.

Zero Footprint

The Zero Footprint team — AI modernisation for Australian logistics.